Adam Memon and the Centre for Policy Studies reckons I’m an Economic Defeatist and that the cuts proposed by George Osborne for the next parliament are “both necessary and feasible“.

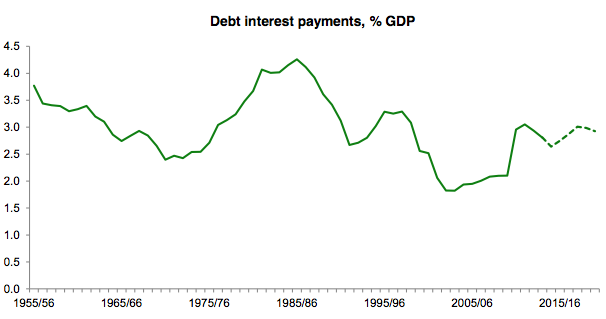

The cuts are necessary, says Adam, because debt interest payments are rising to unacceptably high levels.

It’s true that debt repayments are increasing and they are taking up an ever larger percentage of public spending.

But are they yet at unacceptably high levels?

Not unless they were also unacceptably high under the Thatcher and Major governments. This chart from the parliamentary briefing on government debt, published just before Christmas, shows that, relative to GDP, debt repayments are still lower than they were in the mid 1990s.

Government debt differs from that of households because repayment costs are fixed when the money is borrowed. Any money borrowed now will stay at today’s interest rates. That’s why the government is refinancing all these ancient debts. It’s not actually paying them off, as George Osborne claimed, it’s just redeeming old bonds with new money borrowed at today’s bargain basement prices. Likewise, any borrowing for the next few years is likely to be relatively cheap.

That’s not to say we can ignore government debt. The debt to GDP ratio is almost twice what it was in the mid 1990s and the low borrowing costs won’t last forever. But there is no need to panic about debt repayments at the moment.

Adam also points out that per capita public service spending is only being cut to about where it was at the turn of the century. He says:

Rick seems to counter this by saying that “an ageing population means the number of people needing help from the state is increasing.” However, the two budgets which would most likely see upward pressure from an ageing population are the NHS and pensions; both of which are protected. Demographic change is, for example, quite unlikely to make cutting spending on non-protected budgets such as the Home Office or the Department for Business much more difficult.

That may be true for the Home Office and BIS but it certainly isn’t for local government. Local councils are responsible for social care and residential care for the elderly. They are already diverting funding from other services to maintain levels of care and the ageing population will only add to the pressure.

The NHS has a similar problem. Although it is being given its ring-fenced inflation linked budget increases, its costs have long been rising faster than inflation. Under the current plans, both the NHS and local government will either run out of money or be forced to cut services by the end of the decade. Per capita public service spending of £3,880 (at today’s prices) won’t go as far as it did in 2000.

There is still scope for more efficiency savings, though, says Adam. Indeed there is. The public sector will be under pressure to cut costs for at least the rest of this decade and probably longer. But the amount that would have to be saved to avoid severe service cuts or tax increases is just too big. Even if the public sector were to manage the average 2.3% productivity improvement for the whole economy, it would still be less than half way towards making the savings it needs. In practice, while organisations sometimes make great strides in efficiency, year-on-year productivity improvements of much more than 2 percent across entire service sectors are unusual.

Adam also notes that local authorities have built up reserves. True again but not enough to avoid the need for service cuts. As the Local Government Association said in October, some of this is insurance against unexpected risks like flooding, and much of the rest is already earmarked for investment in efficiency improvements or to soften the impact of cuts. Reserves can only be spent once. The LGA reckons that most of them will have been used up by the middle of the next parliament.

It’s also true, as Adam says, that most people don’t seem to have noticed a deterioration in services. So far, the government has gotten away with its spending cuts. There are signs that people are starting to worry now though.

As a general rule, people’s contact with the the state is inversely proportional to their income and wealth. The richer you are, the less day-to-day interaction you have with the state. The poorer you are, the more likely it is that you or someone you know will have seen services they rely on cut. Now, though, the impact of spending reductions is working its way up the income ladder. People are beginning to wonder whether they will be next.

As Giles says, you can give blood once and be fine. You might even be able to do it again a few days later. If you lose too much blood in too short a space of time, though, your body stops working. There is already evidence of this happening to the state. Some of its extremities, like grant funded charities, have ceased to function. The people they used to help now pitch up at A&E.

To make spending cuts on this scale would mean closing down some parts of the state. With only 1.4 percent of GDP left for everything that isn’t health, education and defence, some services would simply become untenable. Most of the economists in last week’s FT survey don’t believe it’s do-able and neither did most of those polled by the Centre for Macroeconomics before Christmas. Even Conservative council leaders are predicting the collapse of services if the Chancellor’s cuts go through.

This is debate is going way beyond party politics and ideology now. It’s not just the left criticising the Chancellor’s plan. Economists, Conservative councillors, police commissioners and even American generals are picking holes in it too. Make no mistake, the spending cuts implied by the Autumn Statement and outlined in the OBR’s report would, as Paul Johnson said, be colossal. Efficiency savings and council reserves will, at most, provide a temporary anaesthetic before the real pain sets in.

Reblogged this on sdbast.

Rick seems to counter this by saying that “an ageing population means the number of people needing help from the state is increasing.” However, the two budgets which would most likely see upward pressure from an ageing population are the NHS and pensions; both of which are protected. Demographic change is, for example, quite unlikely to make cutting spending on non-protected budgets such as the Home Office or the Department for Business much more difficult.

He’s really missing the point here. The fact that some budgets are protected means that the burden of spending cuts has to fall more heavily on other areas, and the heaver the cuts on those other areas the more difficult it is to make them without a noticeable impact in the services they provide.

Also, spending on health and pensions, along with education, has already increased significantly as a share of GDP since the turn of the century, so pointing out that the Tories spending plans “only” take us back 1999 is not much of a counter argument either – that increase will still need to be matched by equivalent cuts in other areas.

Pingback: Views From The Boatshed

“The cuts are necessary, says Adam, because debt interest payments are rising to unacceptably high levels.” Adam Memon.

Adam may be correct to say what he says, but I am not so sure.

1. Interest payments are a long way off from swallowing up tax receipts. In fact, interest coverage (tax receipts / interest payments) is likely to be 10 times, or even higher. In the corporate world, a ratio of this magnitude would indicate to the analyst that there is not much to worry about. As for companies, as for UK Plc ?. It is an entity’s ability to service its debt that is the key metric. As for households and firms, so it must be for a government.

2. Yes, the government could reduce its interest payments by reducing its borrowing and its spending on public services. Assuming an interest charge of £10 for every £100 borrowed, the public would suffer £100 of “disutility” (or pain) due to spending cuts in pursuit of “gaining” £10 in reduced interest costs. Call me old-fashioned, but this does not seem like good house-keeping. Surely, rationality requires gains to exceed costs? Such a policy resembles a householder abandoning their house so as to get rid of their monthly mortgage interest payments. Not a good idea.

I just wonder whether Adam has thought things through properly.

Actually, I am wrong on point 1 above.

The government’s interest coverage ratio should be its primary surplus / interest payments, which should be greater than one if the analogy to a private firm is to stand. The primary surplus should exclude capex in its calculation as it does for firms (ie a firm’s operating profit).

In the light of so many problems and issues, I cannot understand why both Labour and Tories do not try to get taxes from the ridiculous high housing market (At least from 2nd houses and BTL).

The cuts suggested by both parties might derail the economy so it would have been much better to not have to go though some cuts by using some additional taxes. BTL and property speculators have been able to take advantage of the reduced supply and low mortgage rates while workers-tenants have been suffering. Time to ask the BTL/property speculators to pay something back for their profits subsidised by our government/BoE.

Its called Capital Gains Tax, and it has been tightened up a lot recently.

Actually, HMRC has just launched a campaign to collect overdue/undeclared capital gains tax from buy to let investors. The taxable gains on house sales have been avoided/evaded by many property investors, hence HMRC’s campaign

Pingback: Who is lying about UK budget plans? The OBR test. | Homines Economici

Small point. You mention it’s said people have hitherto not really noticed the cuts. Have you seen road markings recently? Probably not because on my 30 mile drive to work they’re becoming invisible. And I’m not talking minor roads either but anything from motorway junctions down. Small thing but a canary in the austerity coalmine.

Also the holes in the roads, councils just don’t have the money to repair stretches properly, just throw a bit of gravel and tar in and roll it flat-ish.

That debt interest chart shows just how bonkers the 1980’s were – why wasn’t there a popular uprising?

Surely part of Memon’s argument is based on:

” The OBR forecasts that real household disposable income per person will have increased by just over 1% between 2010 and 2015. They also project that it will increase by just under 6% during the next five years.”

Which to me, as an aspiring worker (nobody wants to employ me, despite my experience and qualifications), is totally and utterly bonkers and out of step with the evidence shown on this blog. I guarantee that whilst the average household disposable income might just increase by 6% in the next five years, it’ll be heavily skewed towards the top 0.1 and 1% of the population, with most people no better off.

Reblogged this on Britain Isn't Eating.

Pingback: Hyperbole in politics | Homines Economici

No understanding Rik of how you can suggest that government borrowing differs from household borrowing because of the fixed rates . Seems to me that it’s one of the many similarities between the two . Admittedly one of my lifetimes mortgages varied but others were fixed on the signing of the contract and I later converted the variable mortgage to a fixed when rates fell , just like government debt . The few loans I used for major household purchases were likewise fixed . So apart from the size and the personal responsibility (irresponsibility ?) which politicians don’t have , what’s the difference ? I realise that with fixed rate loans both parties take a gamble on future rates but please don’t even mention the stupidity of credit card or unsecured borrowing .

Why would we need to panic about public debt?

Because it’s ‘public’ meaning it’s your and my debt accumulated over time on our behalf by prudent politicians……nice eh ? But don’t you panic Bob , I’ll settle your share !